📉The stock market fell last week, with the S&P 500 shedding 0.2% to close at 6,025.99. It’s now up 2.5% year to date and up 68.5% from its October 12, 2022 closing low of 3,577.03.

Despite the looming threat of tariffs, the stock market continues to trade near record highs.

This is a bit confounding since tariffs would be bad for earnings, and earnings are the most important driver of stock prices.

Perhaps the market is betting that any tariffs will either be short-lived or less burdensome than feared.

Standing by to revise earnings estimates lower 📉

As we discussed on Monday, the effects of new tariffs on goods imported from Mexico, Canada, and China have not been factored into a lot of companies’ earnings guidance.

While the tariffs on Mexico and Canada have been delayed for a month, they very much remain on the table. So investors should be aware of their potential consequences.

Unfortunately, their consequences go beyond just the direct effects of higher costs on production and higher prices on demand. This makes estimating their full impact on earnings difficult to pinpoint.

“We estimate that every 5pp increase in the U.S. tariff rate would reduce S&P 500 EPS by roughly 1-2%,” Goldman’s Kostin said. “As a result, if sustained, the tariffs announced [on February 1] would reduce our S&P 500 EPS forecasts by roughly 2-3%, not taking into account any additional impact from major financial conditions tightening or a larger-than-expected effect of policy uncertainty on corporate or consumer behavior.”

BofA’s Savita Subramanian estimates: “China+Canada+Mexico tariffs could be as much as an 8% hit to EPS.”

According to FactSet, analysts estimate S&P 500 EPS will grow 13.0% to $272 in 2025 and 13.8% to $309 in 2026. So the announced tariffs could have a meaningful impact on earnings. And keep in mind that President Trump has discussed imposing tariffs beyond what’s been announced.

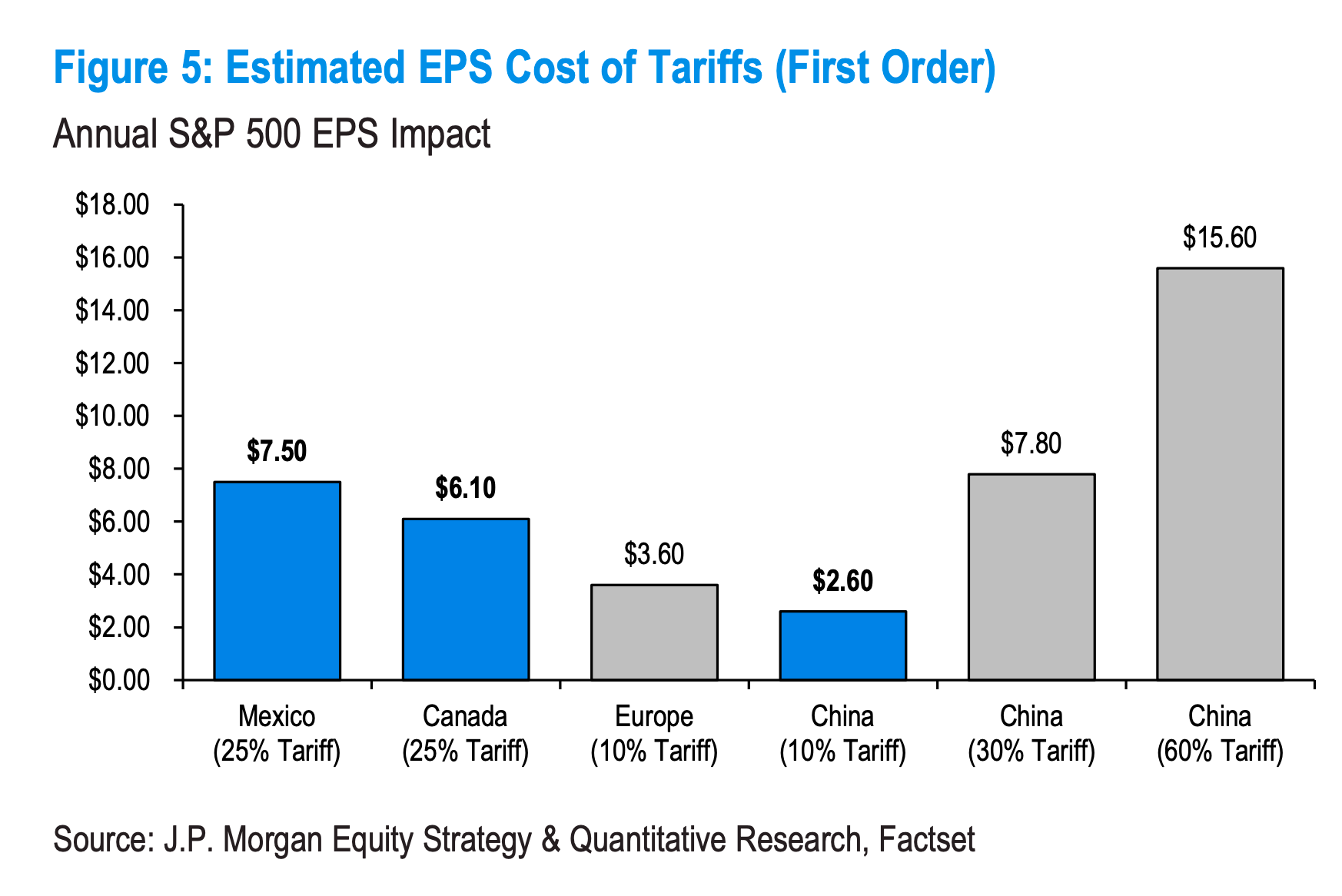

“We estimate that the current tariffs explicitly mentioned could result in an EPS headwind from first order effects of $7.50, $6.10 and $2.60 from Mexico, Canada and China tariffs, respectively,” JPMorgan’s Dubravko Lakos-Bujas wrote. “If we were to presume that Europe would face a 10% tariff, that would be another $3.60. In short, this could impact up to 2/3 of S&P 500 EPS growth this year from just the currently announced tariffs.”

Even if tariffs ultimately aren’t imposed, the uncertainty and volatility caused by the threat of tariffs could prove costly. Among other things, it’s already affecting how importers time their purchases, which can come with higher storage costs and increased risk of inventory held or sold at a loss.

The good news 👍

For now, earnings continue to perform remarkably well.

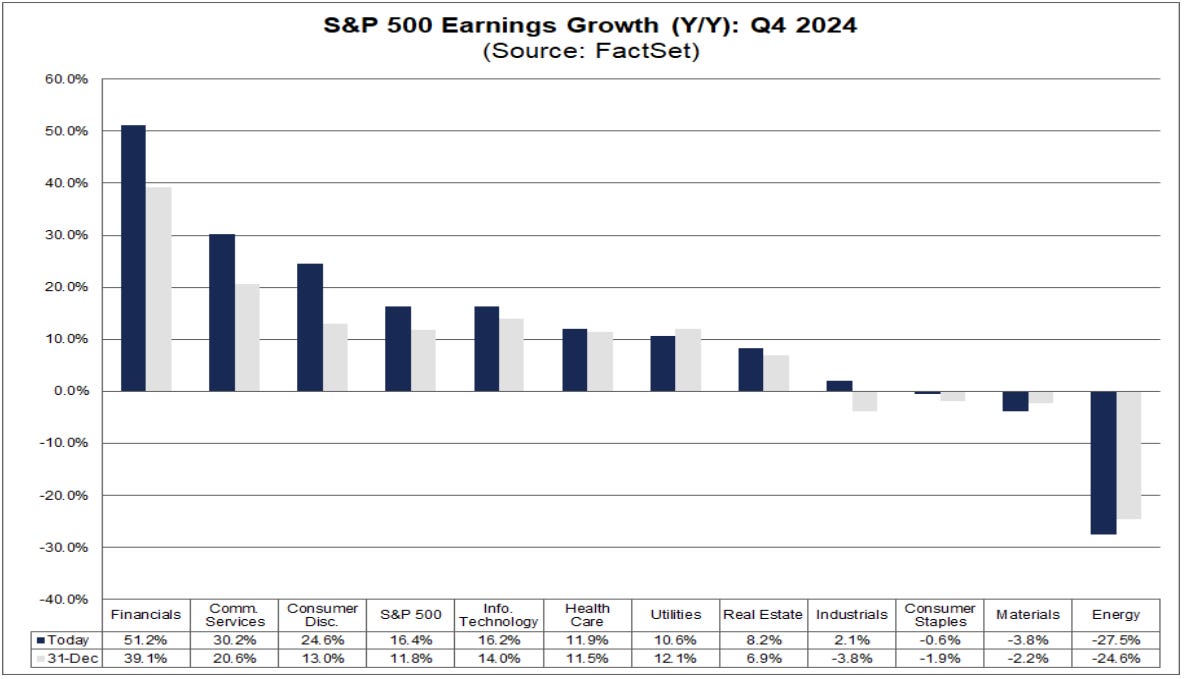

Nearly two thirds of the S&P 500 companies have reported Q4 earnings. According to FactSet, EPS growth is on track to grow by 16.4% year-over-year, the highest growth rate since Q4 2021. This is significantly higher than the 11.8% growth expected by analysts at the beginning of the year.

If this pattern of better-than-expected earnings were to continue — which by the way is one of the most consistent trends in stock market history — then it’s possible that the downside of any tariffs could be at least partially offset by what would be upside surprises in reported earnings.

Subscribed

It’s all about earnings 💰

As I laid out in TKer Stock Market Truth No. 5: “News about the economy or policy moves markets to the degree they are expected to impact earnings. Earnings (a.k.a. profits) are why you invest in companies.”

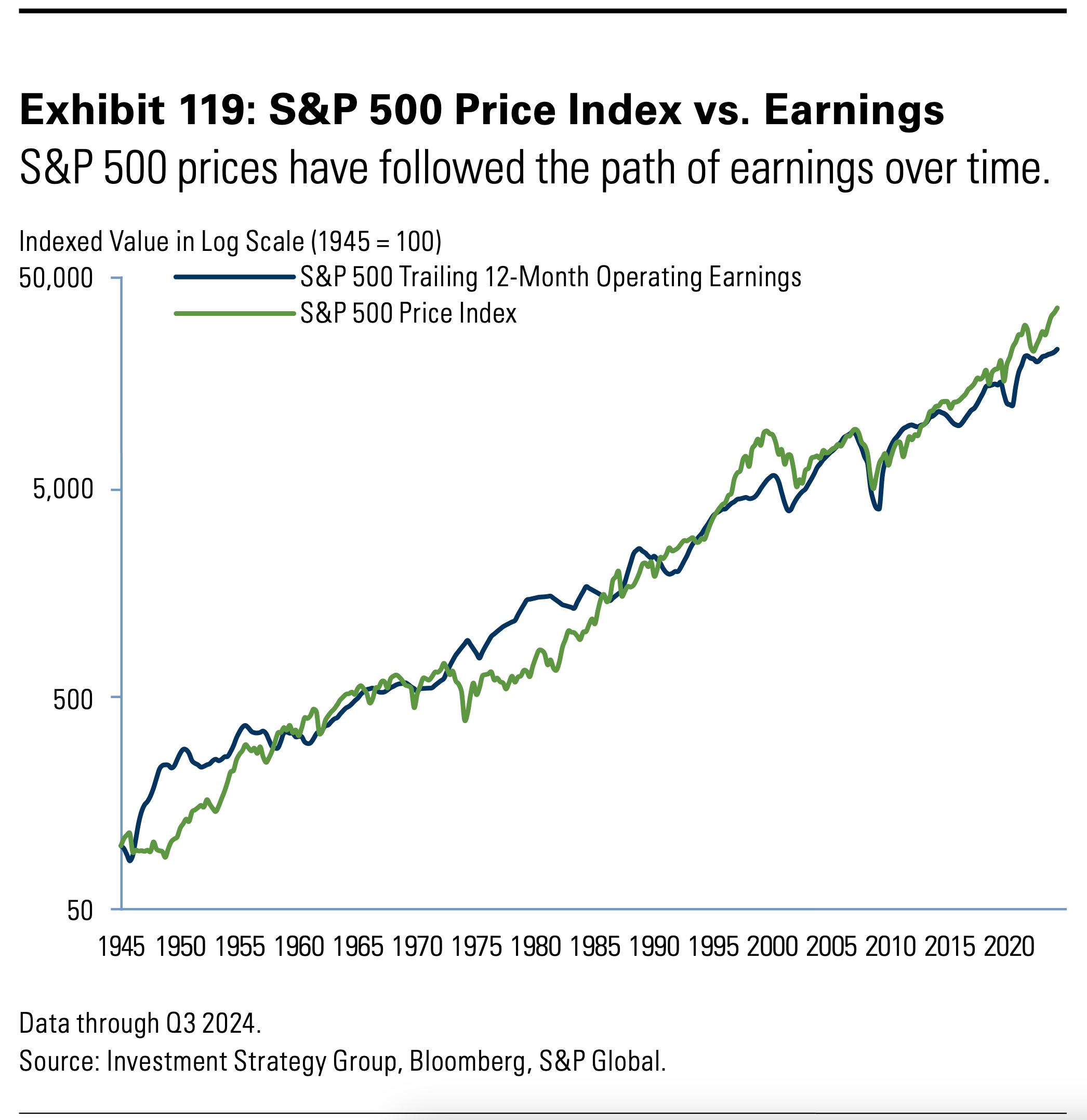

As TKer readers understand, earnings are the most important driver of stock prices. Earnings and prices have one of the tightest correlations of any two variables in markets. Just look at the chart below from Goldman Sachs.

Goldman Sachs explained: “The close relationship between the economy and market performance is largely driven by earnings. Because corporations are paid in nominal dollars, their sales and earnings tend to track nominal GDP growth over time. Rising sales typically boost profit margins as well, since companies often have some fixed costs that do not scale with higher revenues. As a result, margins historically expanded about two-thirds of the time during past periods with positive sales growth. … Given these linkages, the S&P 500 has closely followed the path of earnings over time. Even with significant expansion in the P/E ratio over the last decade, earnings and dividends still contributed three-fourths of the S&P 500’s total return.”

That last point is an important one. As much as we all obsess over P/E ratios, the dominant driver of prices has been earnings not valuations. (Indeed, in the Feb. 07, 2024 TKer, I said that moves in the P/E ratio just reflect the margin of error in what is a very tight relationship between prices and earnings.)

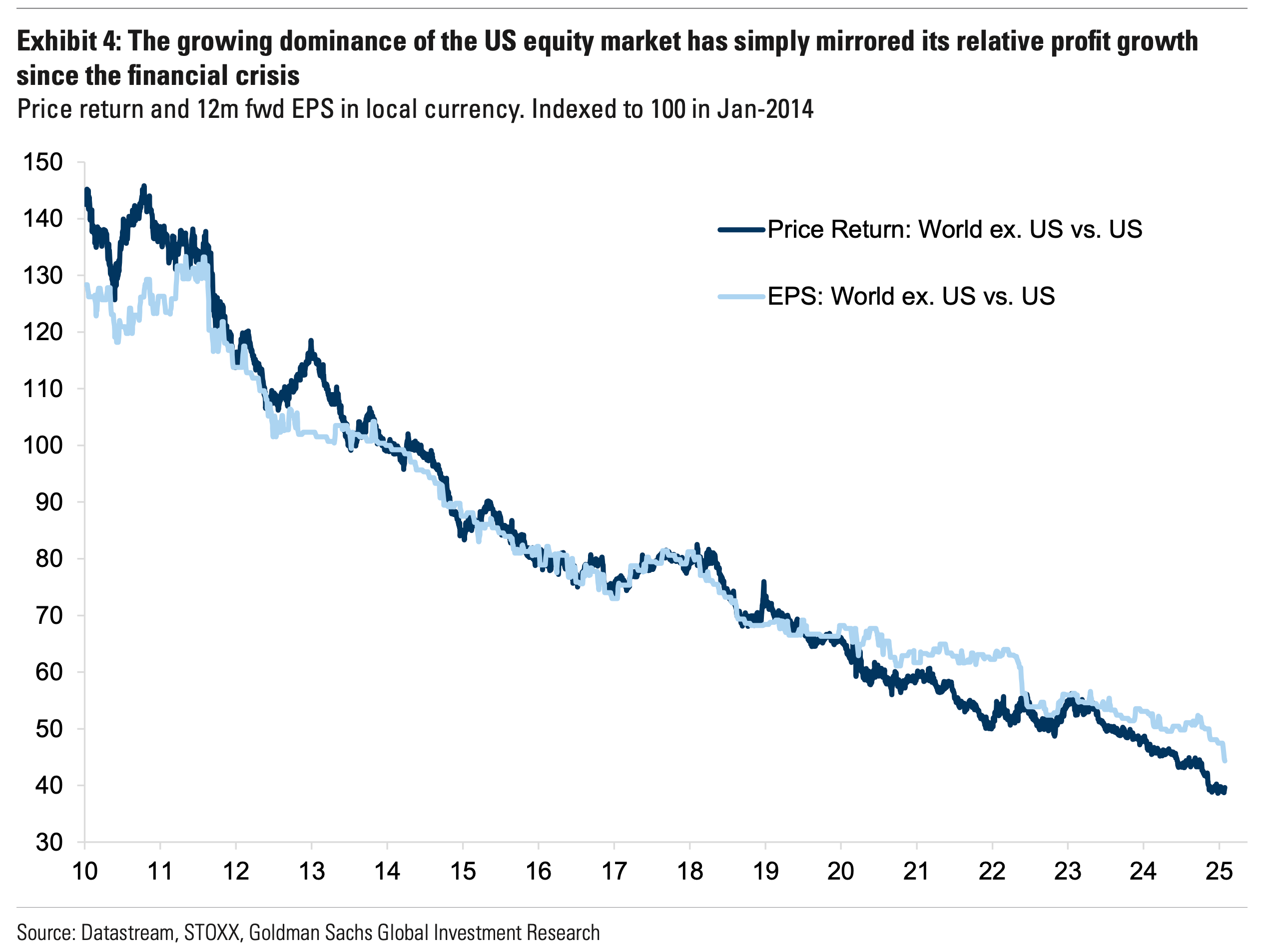

And by the way, earnings explain why U.S. stocks have smoked non-U.S. stocks.

“The growing dominance of the US equity market has simply mirrored its relative profit growth since the financial crisis,” Goldman Sachs’ Peter Oppenheimer wrote.

It’s worth stating that tariffs also hurt the countries on which tariffs are being imposed.

If the trajectory of earnings were to shift due to tariffs, we should expect prices to follow.

Market standoff 😰

Because tariffs are almost universally considered negative for all of the economies involved, their implementation would mean earnings estimates will come down.

For now, most companies and analysts appear to be waiting for something firm before they make any revisions.

The stock market, meanwhile, continues to trade near all-time highs. This seems to reflect investors and traders wagering that new tariffs either won’t come to fruition or they will be benign.

Maybe the market is right to be trading high, and maybe companies and analysts won’t have to cut their earnings estimates. After all, there’s a case to be made that policymakers don’t want to tank the stock market.

In any case: Investing in the stock market would be a whole lot easier if we knew what was to come.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.